Car sales activity during the week commencing June 7th continued at quite a pace and demand remained good for both the new and used car sectors. The fine weather does not appear to have drawn customers too far away from the virtual and physical showrooms, with consistent volumes of both leads and online reservations to keep the sales and fulfilment teams busy.

The new car market continues to suffer with new stock shortages and this lack of stock means the sales focus is moving to used car sales teams where the belief is that there will be the opportunity to make money. The reality is that the lack of used stock coming to the market means that margins are being squeezed as wholesale pricing continues to overheat for some cars. Watching the slow impact on retail pricing is most interesting, as retailers find themselves in the rare and uncomfortable position where they still have some old stock priced well below similar vehicles that have just come from the wholesale market and need a modicum of margin to make commercial sense to retail them, although a small margin is better than having an empty space. However, consumers drive pricing and if used cars sell at the higher price, then the current wholesale pricing will remain robust for the time being.

The burning industry question at the moment is when the consumer demand will begin to slow down, and supply will start to match demand. Until Monday 14th June, there was an expectation of 6 weeks or so until a balance returned, although the latest announcement by the government to delay a full return to normal life for another month and the continued restrictions on foreign travel, realistically mean that consumers will have less to distract them from buying a new or used car. This is good news for the UK economy and specifically the automotive sector.

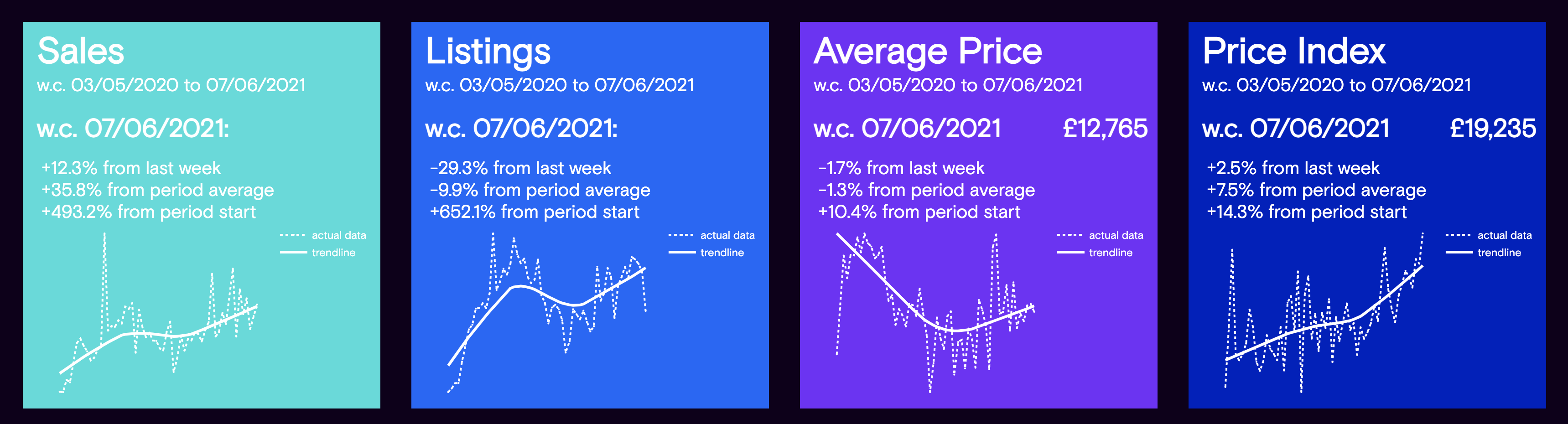

The charts below qualify the market dynamics during the previous week with the full year trend of the data shown at the bottom of each panel: -

Data powered by Cazana.

The data in the charts above is remarkably interesting and shows exactly what happened to the used car market during the week commencing June 7th in comparison to the previous and perceived shorter week, when the Bank Holiday may have impacted business patterns. Day to day volatility remained, but overall an uplift of +12.3% in used car sales was very positive reflecting the continued strength of consumer demand. Of specific note and concern, is what has happened to the volume of new retail listings which dropped by a marked -29.3% on the previous week. It would be comforting to think that this happened due to the slow processing of new vehicles heading for the forecourt as a result of the bank holiday weekend, but the reality is that it was probably due to used car stock shortages.

The Cazana Used Car Retail Price Index increased during the week by +2.5% and took the price to £19,235. When looking at the full year data the index has improved by +14.3% since the beginning of May 2020 and has been more stable in recent weeks than it has been at times during the last 12 months. This higher Cazana Used Car Retail Price Index suggests that there are more later plate cars in the market or perhaps greater analysis of the data will reveal that there are more high-priced premium brand cars in the market pulling the index higher.

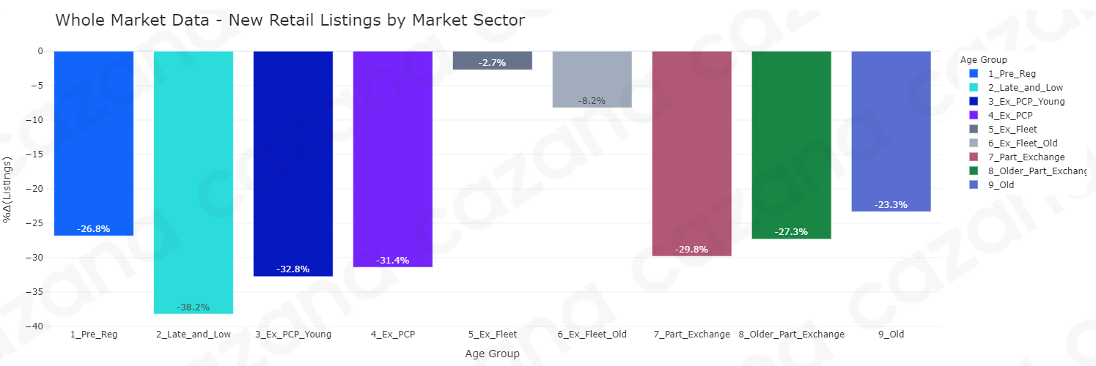

With used car stock shortages causing market concerns of late, a review of the new retail listing information is remarkably interesting and highlights some trends that the market really need to investigate further and consider carefully when looking at stocking and retail pricing policy. The data in the first chart shows that currently new retail advert listings coming to the market dropped noticeably. The chart below looks at this decline in listings week on week by age profile to examine where the potential root problem lay:-

Data powered by Cazana.

It is immediately clear from this chart that Ex Fleet vehicles had consistency in the volume of new listings week on week. The biggest problems seemed to be with the later plate newer cars, where specifically the data saw a drop in new retail advert listings of -38.2% for the Late and Low profile. The largest declines in volumes were categorically reflected in the younger age profiles overall and the question is whether this was due to the drop in availability of new cars boosting sales of used cars that cannot be replaced easily at the moment.

Of equal note is the fact there seemed to be a better supply, if that is what you can call it in a week where new retail listings dipped so far, of Old Car profile vehicles coming to the market. Cars over 10 years of age are an important and considerable part of the used car sector and it is good to see a better volume of new retail advert listings for this area of the market.

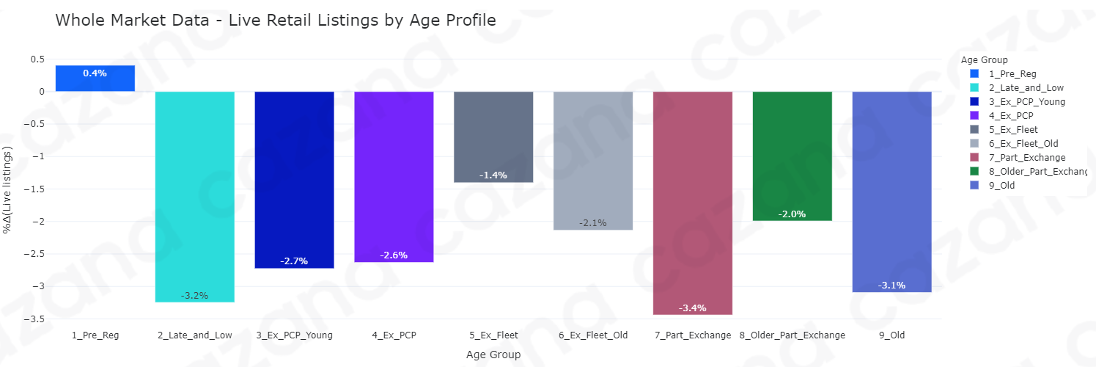

With a different lens the chart below looks at the change in the number of Live Retail Advert Listings week on week. This has been split by Age Profile once again to add context to the previous chart :-

Data powered by Cazana.

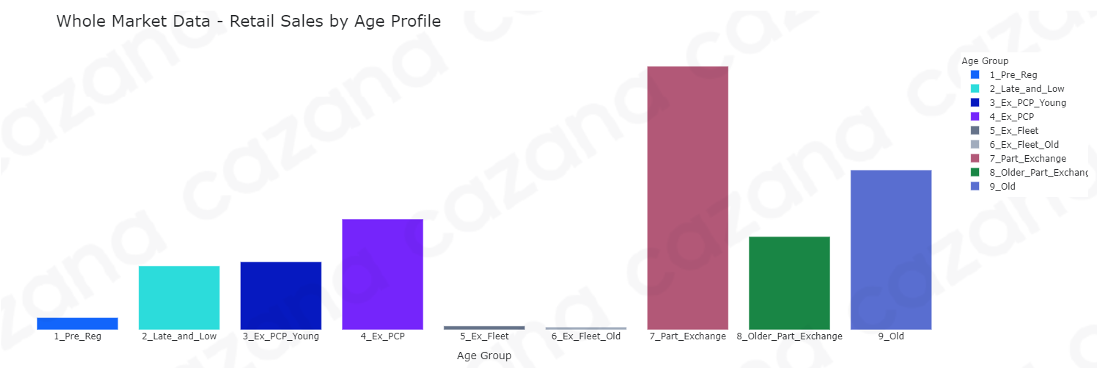

Despite the big decline in the volume of new retail listings, there was more stability when looking at percentage changes in the total number of live retail listings. The data in the chart reflects the move by age profile where the total dip in live retail listings was -2.9%. There is more balance in this data and as such highlights the need to look at this type of insight in more detail on a daily basis to ensure that a complete view of market drivers is understood correctly. The implication of the data at this level is that sales of Late and Low, Part Exchange and Old profile cars were the strongest during the week and this is largely borne out by the chart below showing retail sales by age profile:-

Data powered by Cazana.

Therefore, sales activity in the car market during the week commencing June 7th remained encouragingly good, and this is despite the potential for lower sales volumes as consumers both enjoyed good weather and perhaps looked to spend their money on holidays and other big-ticket items instead. The latest government announcement and the tight foreign holiday green list look set to benefit both the UK economy and more importantly the UK automotive sector in the coming weeks. The data in this Weekly Pricing Insight highlights the need to review daily insight to keep in tune with the swiftly changing market conditions and to have clarity over the pace of retail price movements in relation to wholesale pricing. All may not be as some might show in other areas of the media, and only Cazana real-time retail driven data can give clarity to market performance.