Used car sales activity in the last week has switched once again and whilst consumer demand appears to have remained generally strong, some retailers have reported that the customer commitment levels have dipped, and sales have been harder to close. There has been some feedback that this is due to alternative leisure spending options becoming available in recent weeks, such as foreign and domestic holidays, and these options appear equally appealing as buying a new car.

The national press has also made much of the appearance of the Indian variant of COVID 19 in the UK and the threat that this may have to the “return to normal” plan that the country is currently following. This has led to speculation over whether the retail car showrooms will need to be closed again as part of an extensive program of Local Lockdowns as experienced in late 2020. This is not a desirable outcome by any means and will immediately inhibit retailer sales performance for those affected. With the euphoria surrounding the reopening of the showrooms, this is a timely reminder that the online “mouse to house” solutions developed so hastily last year, really need to remain in place as a valuable consumer purchasing alternative and that open showrooms are not necessarily the panacea to the automotive sector recovery.

The charts below qualify the market dynamics during the previous week with the full year trend of the data shown at the bottom of each panel: -

Data powered by Cazana.

The data in the charts above confirms that there was a drop in recorded sales of -20.6% on the previous week and this is symptomatic of the vibrant yet volatile used car market in evidence since the reopening of the retail car showrooms. Conversely the volume of new retail advert listings increased by +15.8% which although market sentiment shows there is still a restriction on the supply of replacement used cars in the market.

The Cazana Used Car Retail Price Index has decreased marginally by -0.5% and in doing so partly redresses the gain of +1.1% from the previous week. When looking at the period from the beginning of April 2020, the Cazana Used Car Retail Price Index has increased by a considerable +17.2% to £18,555. This lens on the market retail pricing is more positive than that of the Average Retail Price of a car which in the last week increased by 3.4% to £12,721 with a more conservative uplift of +8% since the data period start date.

What is of marked concern is the excessive and short-lived wholesale data pricing peaks that are being experienced when retailers are looking to buy replacement used car stock. In some cases, impatience and buying cars that have already been pre-sold has resulted in significant and exceedingly short-lived spikes in pricing. This is a dangerous period, and it highlights the need for whole market, real-time, retail driven data as provided by Cazana, rather than trying to use auction or individual retail advertising platform-based solutions that can be both out of date and also representative of a much smaller proportion of the used car market.

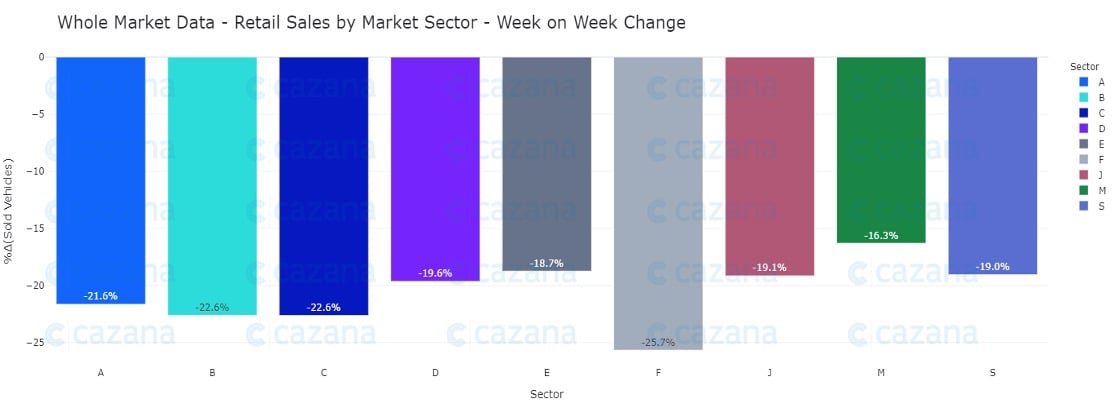

Looking at the market position in a little more detail, the chart below puts a lens on sales by market sector week on week: -

Data powered by Cazana

This chart seeks to establish whether there has been a specific drop in demand for any particular type of car by market sector. Whilst it is not good news to see a market decline overall, the positive view here is that there is reasonable consistency across the market sectors week on week. J Sector SUVs have fared better than all other sectors with F Sector Luxury cars hit worst with a decline of -25.7% and that means that whilst sales activity is volatile, there is no specific area of concern. The drop in sales is in all likelihood just part of the tumultuous post lockdown market.

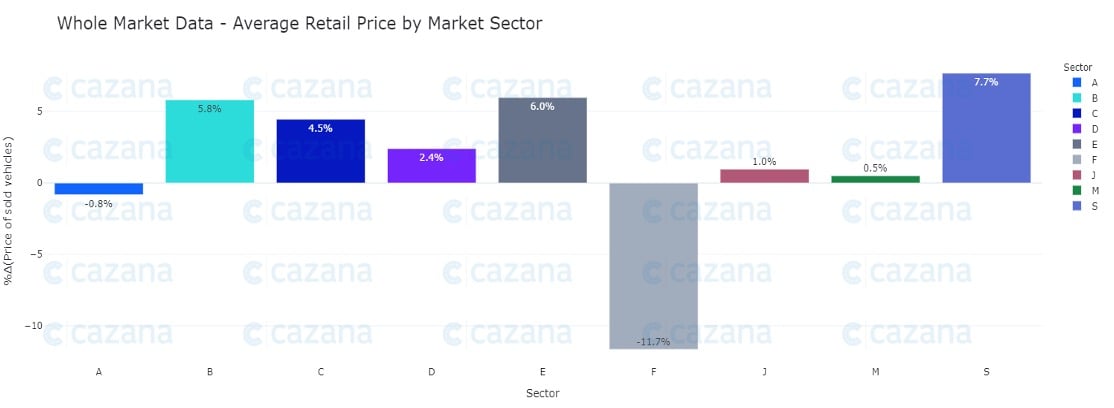

In reviewing the market in more detail and looking at retail pricing performance by market sector, there was movement of specific note in a couple of categories and the chart below highlights the market performance week on week: -

Data powered by Cazana.

Whilst the majority of the market sectors reflect a reasonable delta of movement, there are 4 that show marked change. The obvious move is that for F Sector or Luxury Cars that shows a downward shift in average retail price of -11.7%. This change took the average retail sale price of Luxury cars across the whole market and of any age to £11,657. However, sales of this type of car reflect just 0.6% of the total market share and due to the nature of the sector the removal or sale of a few high value cars can have a significant impact on the data average. Of more reasonable note is the retail price movement upwards of +7.7% for the S or Sports Coupe market sector and +6% for the E Sector Executive cars age profile with a +5.8% gain for B sector small cars.

Therefore, the last week has not performed with the sales volume consistency that the retailers crave as they drive recovering business models to greater success in this post lockdown period. The used car sales volatility is alarming, but at this stage not of major concern. It does serve as a reminder that the retail consumer can be a fickle beast, and also that the automotive industry must not take it for granted that this pent-up demand currently driving retail used car sales can be truly relied upon. Understanding the full market with Cazana’s real-time retail driven insight is the most efficient and effective way of keeping business and commercial strategy in line with market developments.